Trends Analysis of the Israeli market for new vehicles - Q4 2024

January 29, 2025

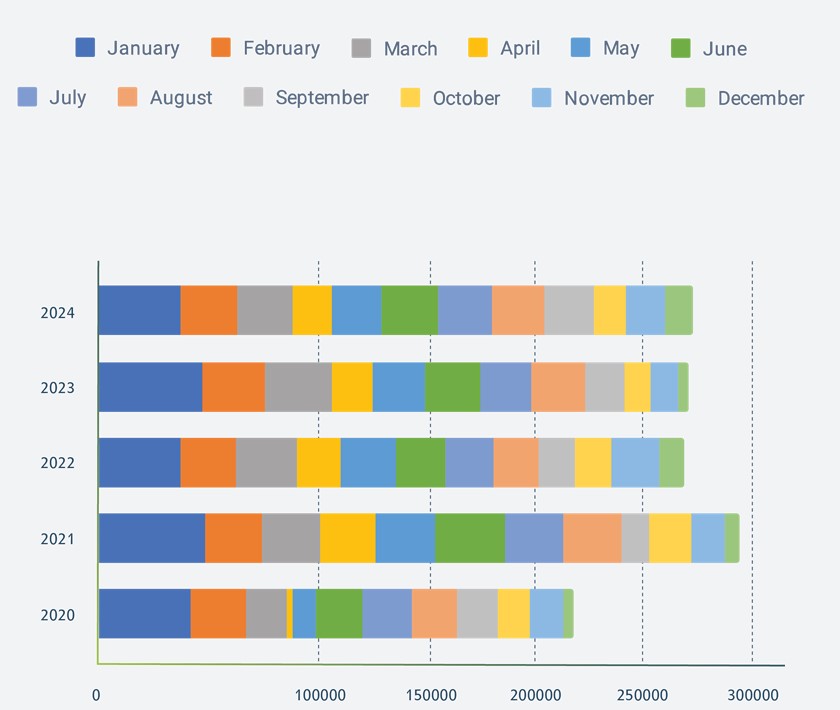

Registration Data

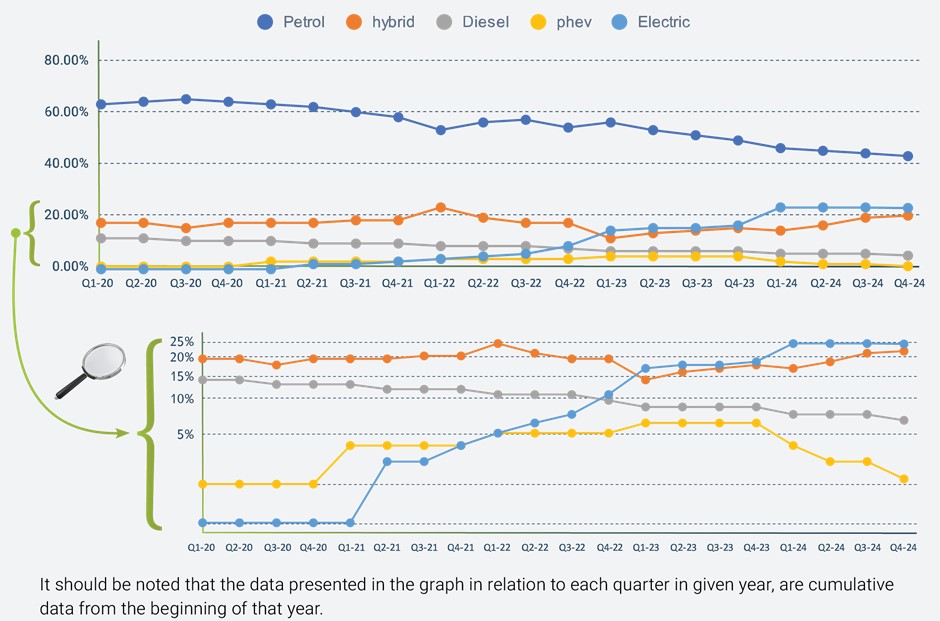

Registration by Engine Type

Petrol vehicles have continued their declining trend, with a reduction from 46% in Q3 2024 to 44.9% in Q4 2024, and a significant drop from 51.4% in Q4 2023. This is part of a broader, steady movement away from petrol vehicles, which have seen their market share decrease from 65% at the start of 2020 to under 50% by the end of 2024.

Conversely, Electric vehicles (EVs) demonstrate the most substantial growth among all types, though they actually show a slight decrease from 25% in Q3 2024 to 24.8% in Q4 2024. Despite this minor quarterly fluctuation, there has been a significant increase from 17.8% in Q4 2023. The rise from just 1% at the beginning of 2020 to nearly a quarter of the market by the end of 2024 underscores a pronounced shift towards electric mobility.

Hybrid vehicles, after experiencing some fluctuations over the years, show a resurgence in Q4 2024, rising to 21.8% from 20.6% in Q3 2024, despite a dip to 17% in the same quarter of the previous year.

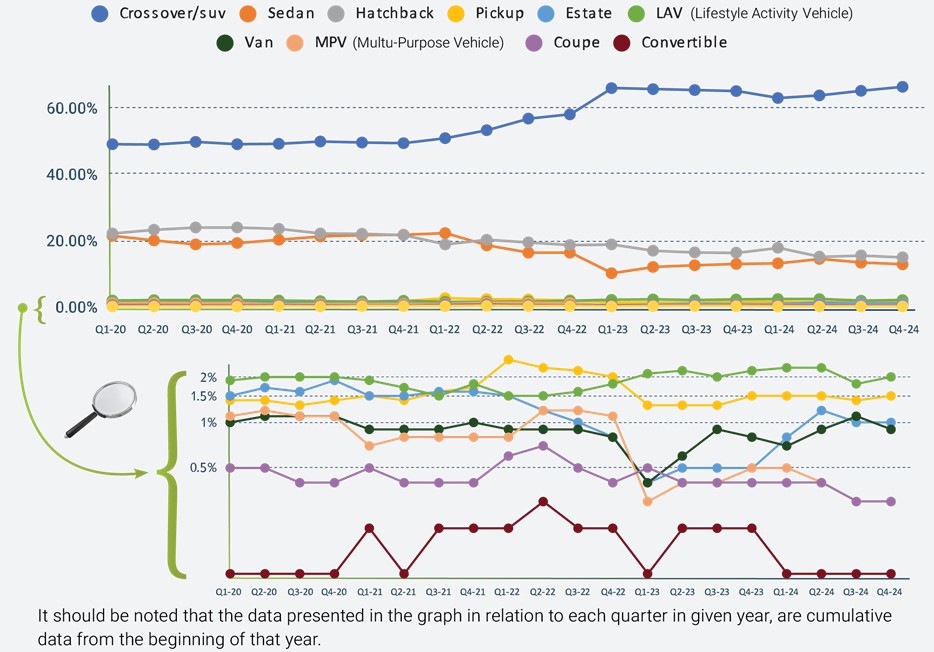

Registration by Segment Type

Crossover/SUVs have consistently grown in popularity, with their market share steadily expanding over the years. By the last quarter of 2024, they accounted for 66.3% of the market, slightly up from 65.1% in the previous quarter and also showing an increase from 65% in the same quarter of 2023. This growth from 49% at the beginning of 2020 highlights a strong consumer shift towards larger, more versatile vehicles.

In contrast, the Sedan segment has been gradually declining. By the end of 2024, Sedans held only 12.8% of the market, a slight decrease from 13.3% in the previous quarter and down from 12.9% in the fourth quarter of 2023. This trend represents a significant shift from 21.40% at the start of 2020.

Hatchbacks have also experienced a decline but have shown some resilience in market preferences. They captured 14.9% of the market by the end of 2024, slightly down from 15.5% in the third quarter and from 16.3% in the same period in 2023.

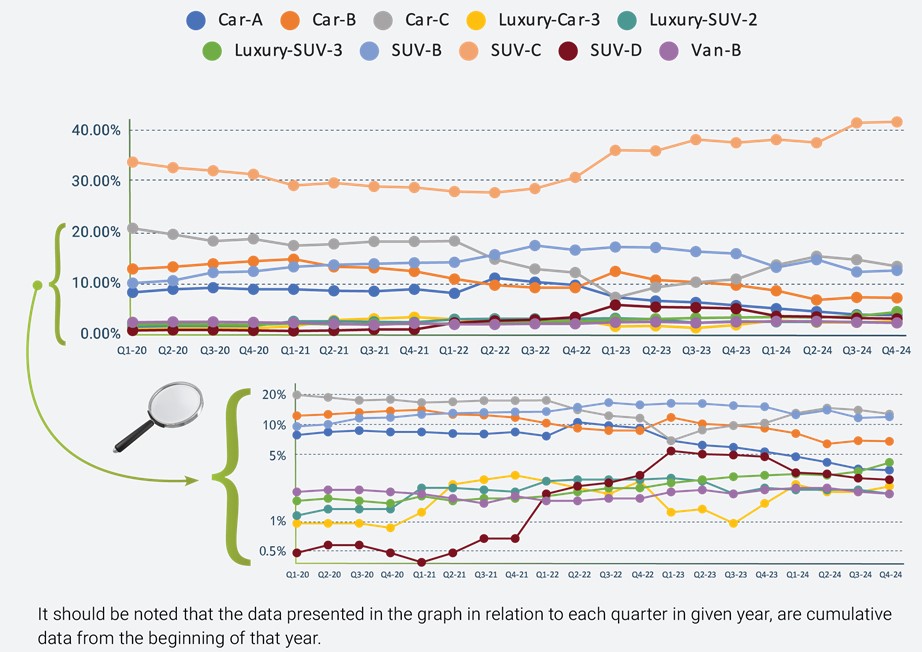

Registration by Category

In Q4 2024, SUV-C remains a strong market leader, capturing 41.5% of the market. It is increasing slightly from 41.3% in the previous quarter and showing a significant growth from 37.4% in Q4 2023. Over the years, this segment has steadily increased from an initial 33.6% in early 2020. The growth trajectory became particularly noticeable in the beginning of 2023, when consumer preferences strongly shifted towards larger, more versatile vehicles, accelerating the segment's growth beyond the general upward trend.

The CAR-C category, on the other hand, has faced a general decline. In Q4 2024, it accounted for 13.1% of the market, recovering from 10.6% in Q4 2023, but still significantly lower than earlier years, starting from 20.6% in 2020. The segment's decline was most pronounced between 2021 and 2022, indicating a broader shift in market preferences away from traditional sedans towards SUVs and crossovers.

The SUV-B category accounting for 12.3% of the market in Q4 2024. This is actually an increase from 12% in Q3 2024 and a decline from 15.6% in Q4 2023. Starting from 9.8% in 2020, the category saw an increasing in interest, particularly peaking in mid-2023.

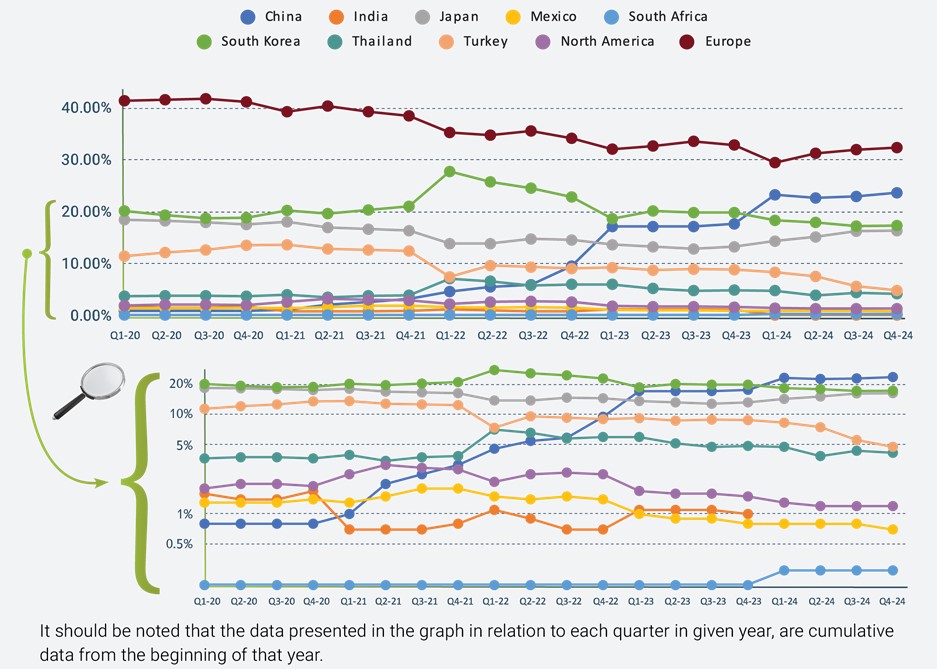

Registration by Country of Origin

Over the years, the market share for European vehicles has generally shown a decreasing trend. In Q4 2024, these vehicles captured 32.2% of the market, slightly down from 32.7% in Q4 2023. This decrease continues the pattern observed from earlier years, indicating a gradual erosion of market dominance.

The trajectory for Chinese-built vehicles has been markedly upward, highlighting their growing influence in the automotive sector. Starting from a lower base in the early 2020s, the market share for Chinese vehicles increased to 23.5% by Q4 2024, up from 22.8% in Q3 2024 and from 17.5% in Q4 2023. This consistent growth underscores China's expanding role as a major automotive manufacturer.

South Korean vehicles have shown some fluctuation but generally depict a slight downward trend in market share. By Q4 2024, they accounted for 17.2% of the market, decreasing from 19.9% in Q4 2023 and 17.1% in Q3 2024.

In Q4 2024, Japanese vehicles held 16.2% of the market, which represents a significant rise from 13.1% in Q4 2023. However, this is still lower compared to Q1 2020, when they had a market share of 18.3%.